W4 Form 2018 Printable

Home

Top Forms

W4 Form 2018 Printable

Home

Top Forms

Get

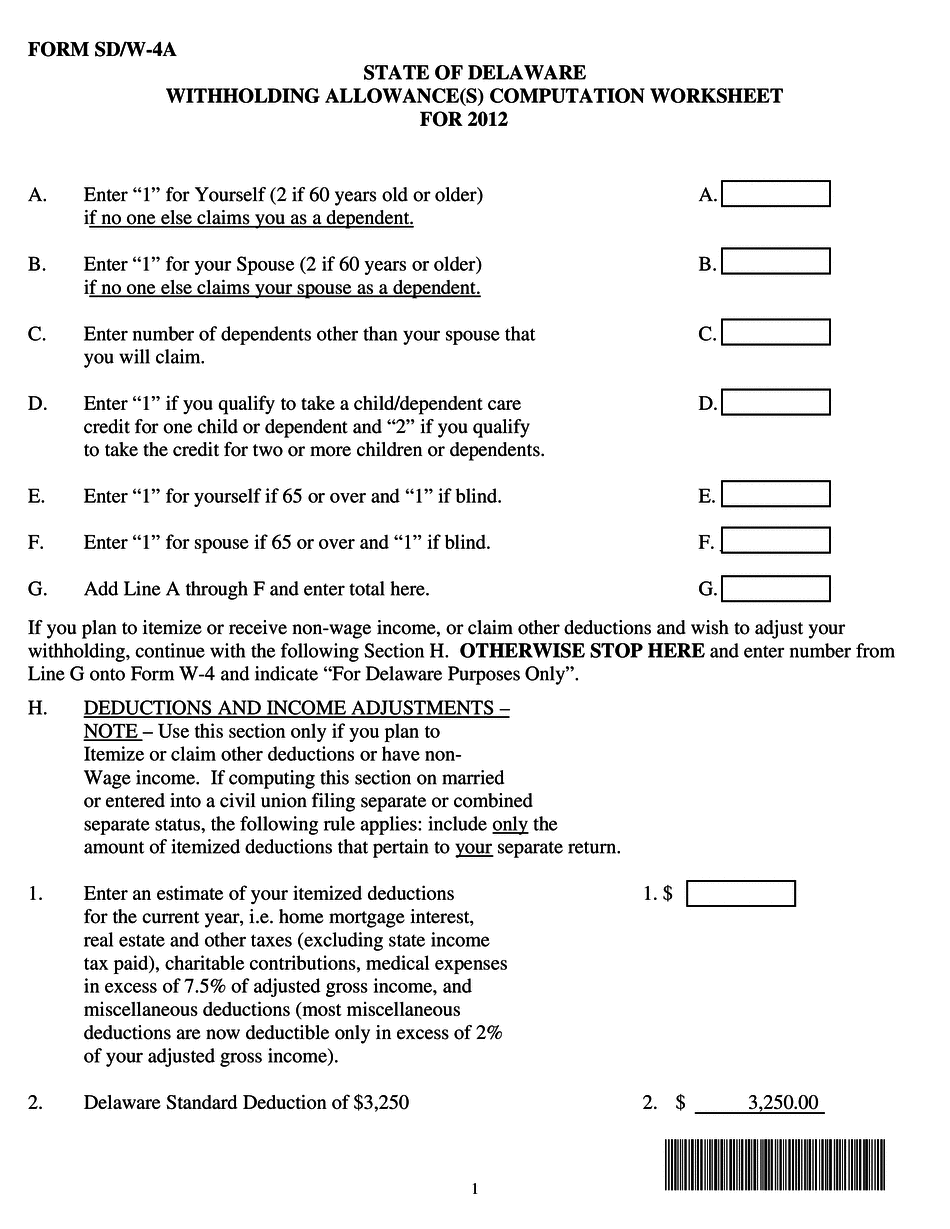

Delaware Form SD/W-4A 2025

Get Form

Home

TOP Forms to Compete and Sign

Delaware Form SD/W-4A

👉

Did you like how we did? Rate your experience!

Rated

4.5 out of

5

stars by our customers

561

Award-winning PDF software

Video instructions and help with filling out and completing Delaware Form SD/W-4A

Related Links

IA W-4 2015-2018 Form

KW-3 Form KS

If you believe that this page should be taken down, please follow our DMCA take down process

here

.

Related Content - Delaware Form SD/W-4A

Forms & Instructions | Internal Revenue Service

Aug 6, 2021 — Complete Form W-4 so that your employer can withhold the correct federal income tax from your pay. Form W-4 PDF. Form 1040-ES. Estimated Tax ...

(IRS) Form W-4 - Prior Year Products

Form W‑4Employee's Withholding Certificate2022Form W‑4Employee's Withholding Certificate2021Form W‑4Employee's Withholding Certificate2020Form W‑4Employee's Withholding Allowance Certificate2019View 116 more rows

Form W-4 - Wikipedia

Form W-4 is an Internal Revenue Service (IRS) tax form completed by an employee in the United States to indicate his or her tax situation (exemptions, ...

Get Form

100%

Loading, please wait

.

.

.